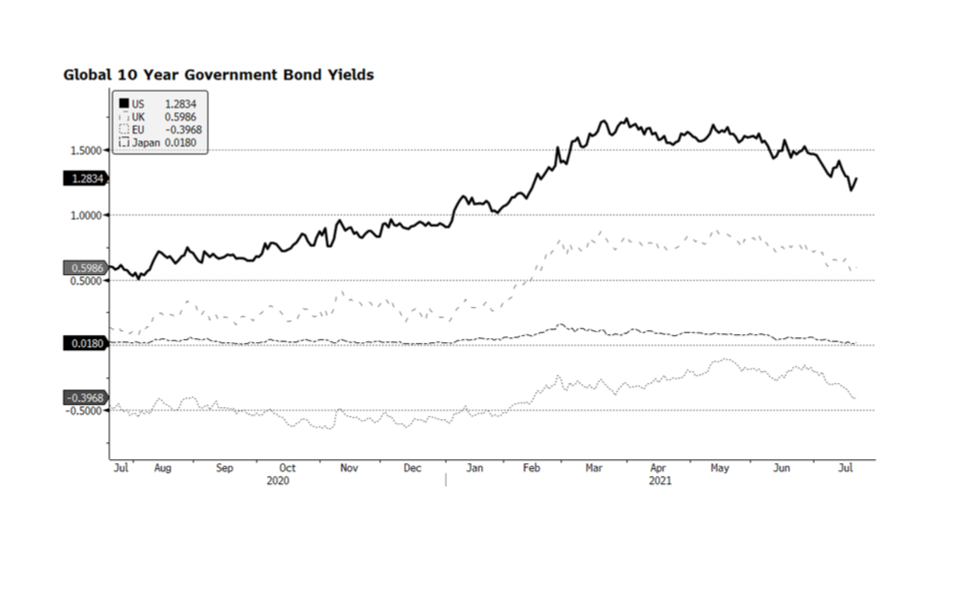

Because we took a hiatus for the holidays, we have extra thoughts to share. The US Bureau of Labor reported that consumer and producer prices came in higher than the consensus last week and that may have been part of the reason why stocks retreated. We view the consolidation in US stocks as healthy at this point, especially considering strong corporate earnings momentum and analysts increasing their earnings forecasts rather than the opposite, which oftentimes occurs at this point in the year. Forecasters usually have a difficult job but given the condition of the world during the pandemic and the incongruent economic recovery so far, it makes now even more challenging. Global bond markets are suggesting a different read on inflation and the near-term outlook for monetary policy, both benign for risk assets. The benchmark 10-year US Treasury bond yield continues its decent after the near-term peak of 1.74% on March 31st and now at 1.28%. Interestingly, government bond yields in the developed world have also fallen with equivalent US interest rates suggesting that current inflation readings are more of a temporary condition rather than a long-term concern. Disinflationary trends are starting to emerge including declining commodity prices, benign capacity utilization rates and strong productivity levels. If bond yields were trending higher along with stronger inflation readings we would be more concerned about risk assets. [chart courtesy Bloomberg LP © 2021]