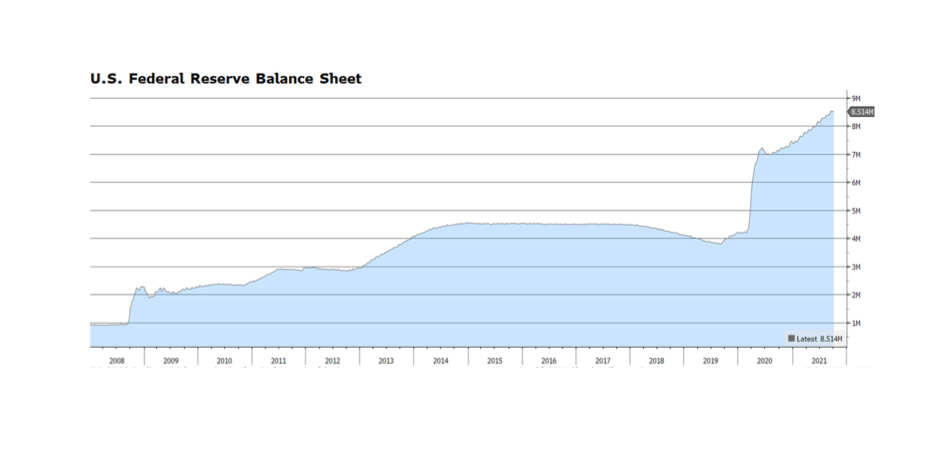

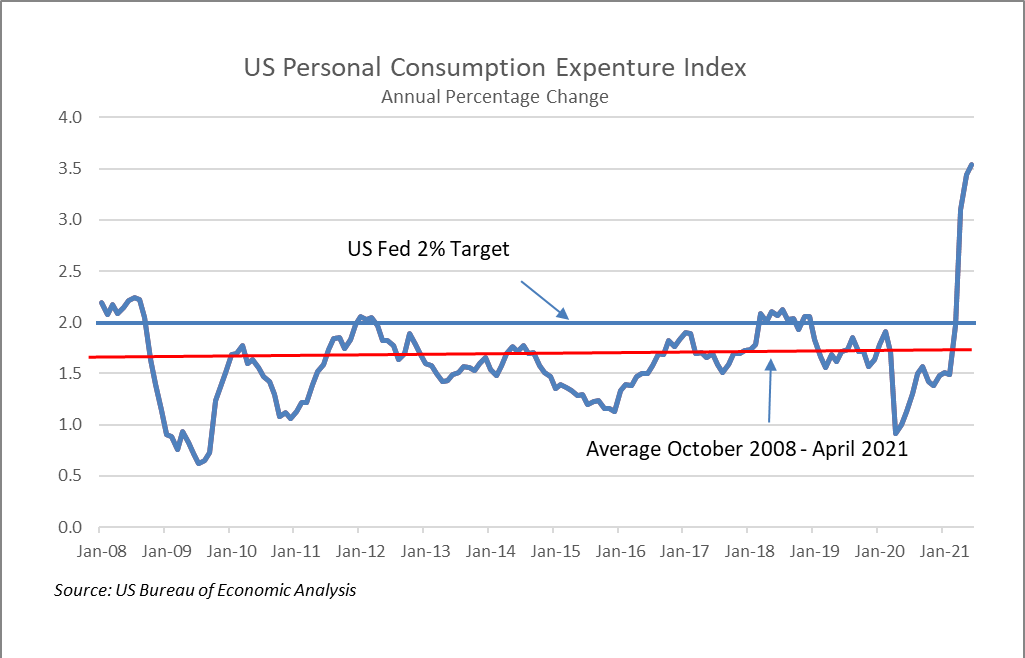

The US Federal Reserve balance sheet currently stands at $8.51 trillion, doubling in size since the pandemic began. The Fed has recently suggested that it may begin to taper the current $120 billion monthly purchases of Treasuries and mortgages as soon as the November 2nd-3rd meeting. Progress in employment is a potential trigger cited by Chairman Powell for tapering, even considering September’s lackluster jobs report. It is important to note that the Fed will likely continue to expand the balance sheet. What they are talking about is lowering the amounts of new monthly purchases over time, so expanding less fast. Still, a reduction in monetary liquidity. Of bigger concern are the inflationary trends that may force the Fed to introduce less accommodative or even restrictive monetary policy. Prices seem to be increasing nearly everywhere, from energy to food to wages, and the Fed’s preferred inflation gauge, the PCE Deflator, is up 4.3% year-over-year as of August. A combination of higher policy rates and lower liquidity would pose a serious challenge for capital markets. [chart courtesy Bloomberg LP © 2021]