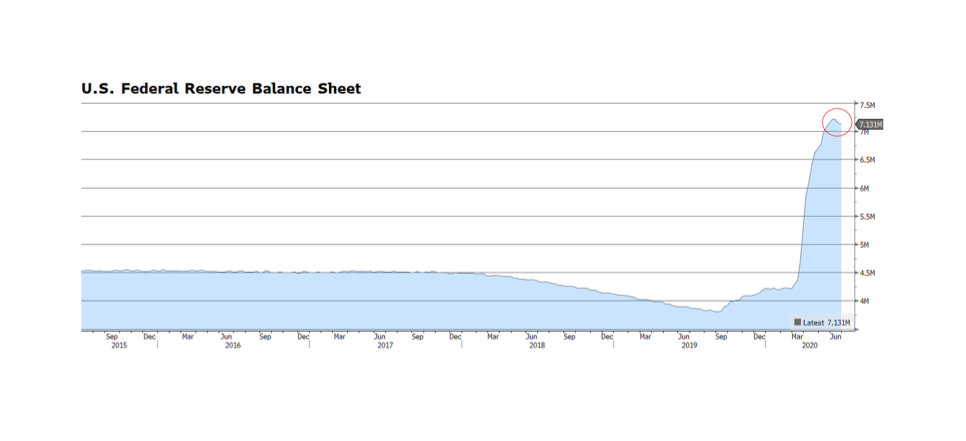

The US Federal Reserve has used the power of its balance sheet to support key segments of US capital markets since early March. Recently, it began to purchase corporate securities including high yield bonds, a move some view as controversial. However, purchasing investment grade (and below) bonds essentially supports companies and ultimately jobs, and full employment is a critical element of the Fed’s mandate. Another beneficial aspect of these purchases is that corporations are making coupon payments and returning principal to the Fed, and that is not necessarily the case with US Treasury purchases. In June, the balance sheet began to shrink, albeit modestly. It peaked at $7.22 trillion on June 10th and currently stands at $7.13 trillion. Following two consecutive weeks of balance sheet declines, stocks have fallen 5.3% as measured by the S&P 500 through June 26. News headlines cite the rise in COVID-19 cases as the reason for recent stock market volatility, but the Fed’s purchasing activity is likely a greater fundamental force dictating the direction of asset prices. Is this a pause or the beginning of a monetary policy tightening cycle? The state of the Fed’s balance sheet is a critical metric that we will continue to monitor. [Chart courtesy Bloomberg LP © 2020]