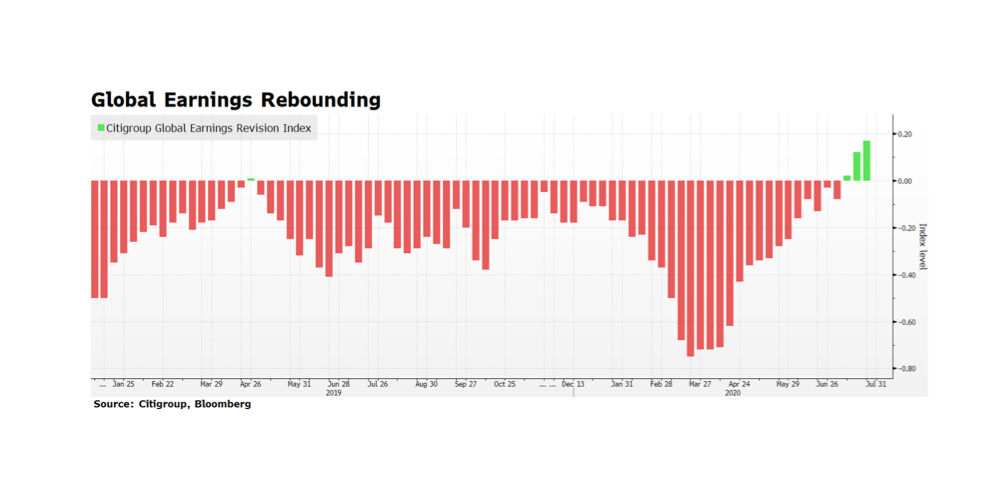

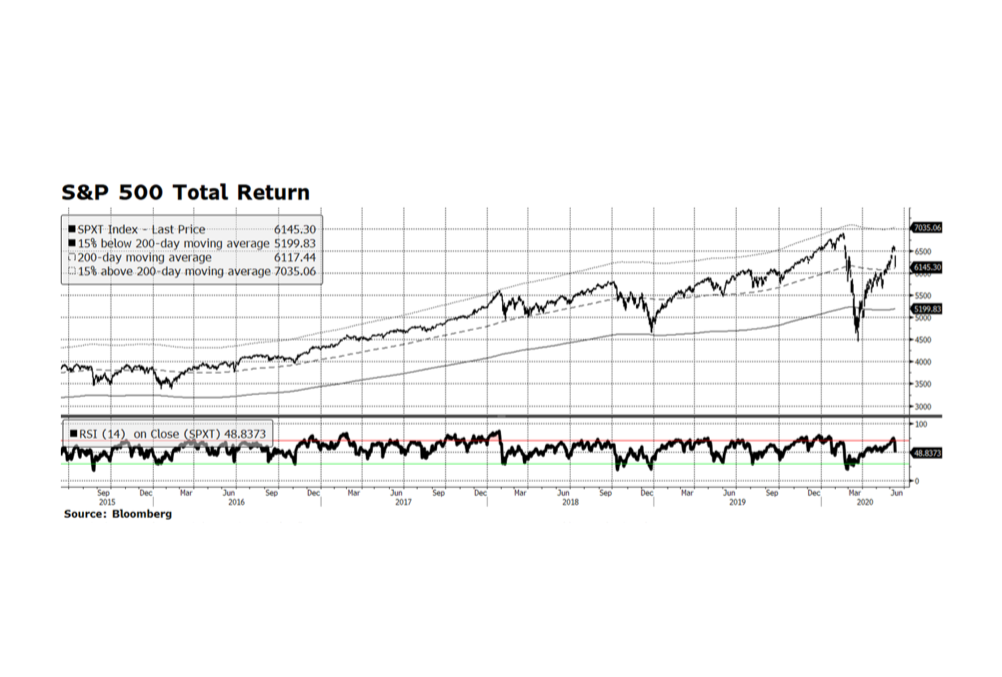

Over the past few weeks, corporate earnings across the globe have been showing signs of recovery. Citigroup’s Global Earnings Revision Index has been climbing for three weeks in a row, encouraging given the economic challenges facing the world. While this trend is positive, its path will be unpredictable due to COVID-19 related shut down and re-openings in several key economies. The recovery in corporate earnings, if it persists, could alleviate the tragic stress in labor markets and help reinvigorate economic activity heading into 2021. Fiscal support is building momentum with the European Union’s 750 billion Euro stimulus plan (discussed last week) and the anticipated fourth phase of US stimulus. It does remain to be seen if the enormous amount of spending, both fiscal and monetary, will have a lasting impact.