That is the question. Whether ’tis nobler in the mind to suffer the slings and arrows of outraged citizens, or to take votes against a sea of troubles, and by opposing end them?

We have been watching this theatre of the absurd since the exit vote passed, with calumnies hurled back and forth, plans drafted and shredded, ministers appointed, ministers departed, political lines in the sand drawn and redrawn, and no actual progress on either following or revisiting the will of the people. Parliament is so feckless they cannot pass a vote to move in any direction, nor can they muster the support to remove the leadership and try something else. Fortunately for the markets, even with trouble looming on the horizon, the net of doing nothing is that the status quo remains. It appears March 29th will come and go without any action beyond resolving the intent to plan for a discussion about the plan. Monty Python could not have written it better.

What to do?

There is simply no way the UK is going to stumble toward Brexit without some form of roadmap in hand. There are too many unmanaged and ugly consequences otherwise, from re-establishing a hard border between Ireland and Northern Ireland to trading internationally, even across the Channel, with no trade accords. With various structural events between now and Summer including the EU parliamentary elections in late May, there are plenty of reasons and plenty of opportunities to do something, even if that something is to resolve to do nothing. It may be that staring into the abyss is enough to compel the UK and the EU to address the Queen’s subjects’ major concerns around immigration, home-rule, etc. through the parliamentary and rulemaking process and belay or even ultimately put aside an exit. It could also be that the UK finds a way to rescind Brexit through whatever constitutional means are at their disposal.

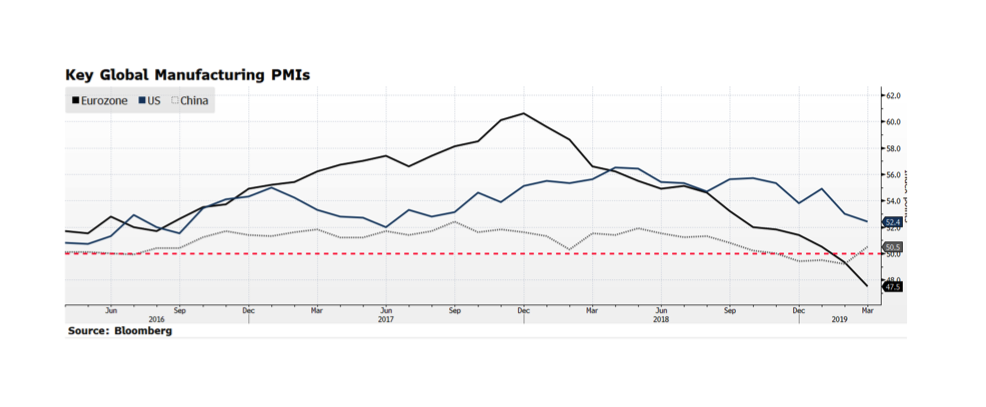

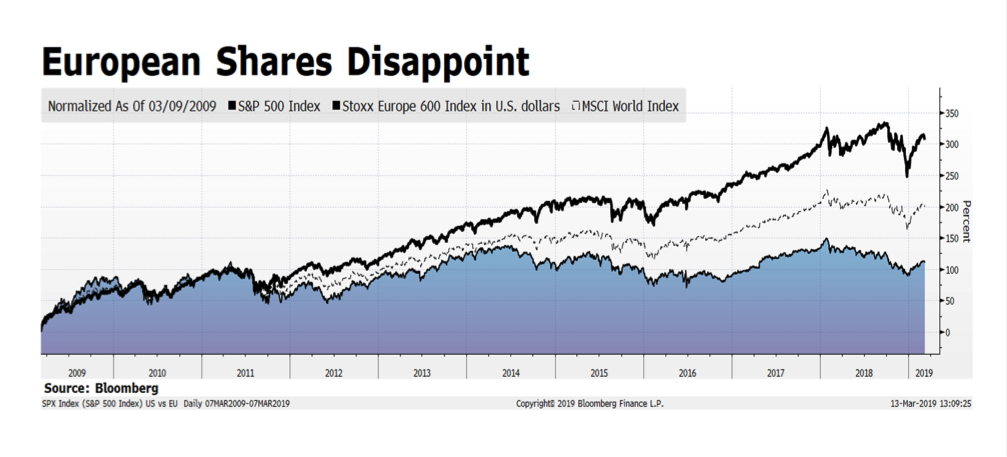

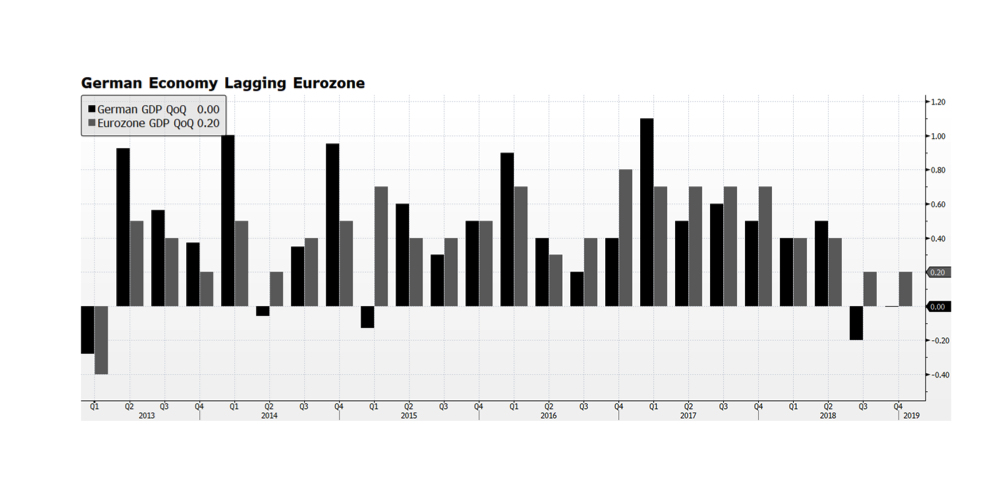

But what if they do stumble out the door with no plan or path? It would be ugly and intensely unpleasant for everyone and may re-open old geopolitical wounds, but the free markets will price the new reality and, as the Brits say, carry on. We have seen a threat to asset prices in the UK and EU and have been significantly underweight relative to our policy benchmarks, although not exclusively for those reasons. Europe appears to be sputtering, including in economic powerhouse Germany, which has given us ample reason to believe the near term opportunities for investors are in North America and Asia. If the UK gives Europe Her Majesty’s middle finger, that could unleash instability and a repricing as markets try to find a new equilibrium based on conditions that have not existed since before many market participants got their educations and first jobs.

What we can do right now is watch closely. A disorganized Brexit could send markets into a period of significant turbulence. An orderly and well structured Brexit, or even no Brexit at all, could potentially herald a new moment for stability and growth and a reason to consider reinvestment in the region.