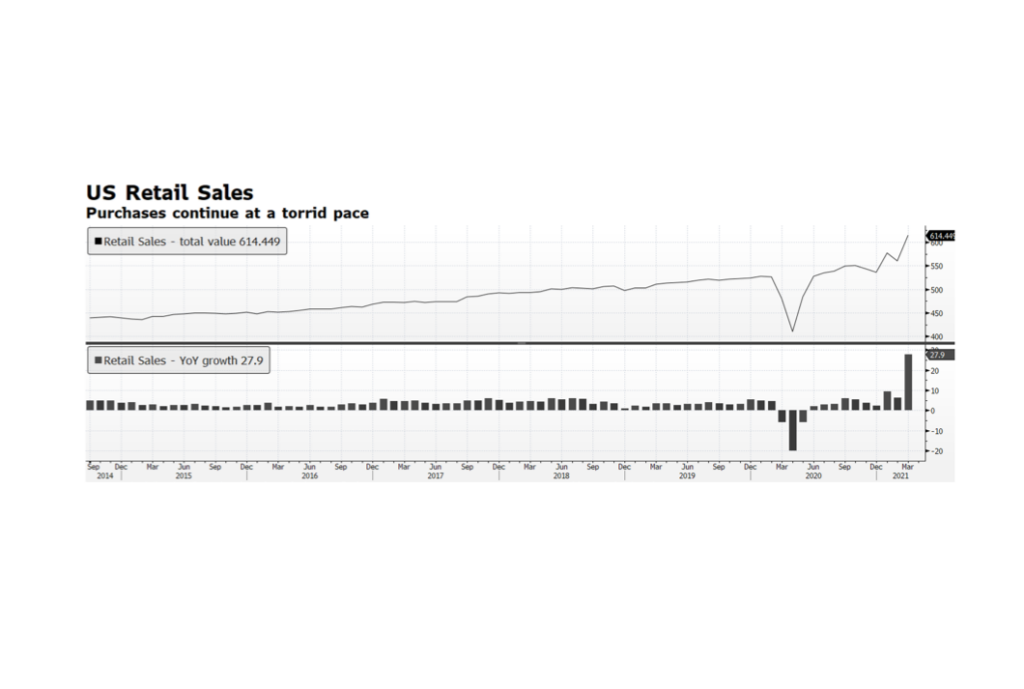

The US Census Bureau’s latest survey of retail sales will be reported on May 14th. The Bloomberg survey of economists’ average forecast is for a 1.0% monthly gain, adding to March’s torrid 27.9% annual pace. March’s level of over $614 billion in purchases is nearly 17% higher than the pre-pandemic level of $525.8 billion of February 2020. Consumption, the most dominant portion of the US economy, is clearly rebounding and could further stoke inflationary concerns. This is occurring as hundreds of billions of US fiscal stimulus dollars have yet to be fully deployed with potentially more on the way on top of elevated commodity prices, shortages in building materials and the labor force far from full employment levels. The Fed remains committed to QE, in effect managing the entire yield curve, and has publicly stated that it will tolerate higher inflation. But for how long? Market pressures may force the Fed to act sooner than they currently plan and that could be a major shock to the system. [chart courtesy Bloomberg LP © 2021]