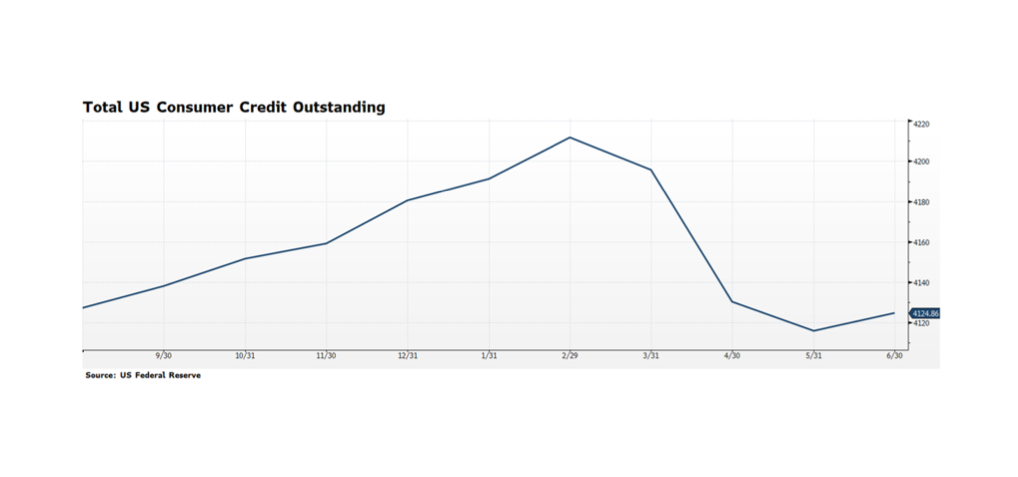

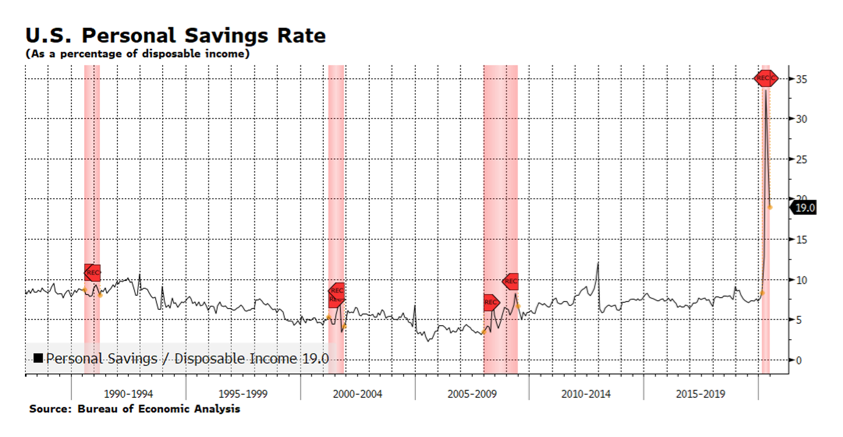

A few weeks ago we discussed US consumer trends, citing the elevated personal savings rate as reported by the BEA, in addition to citing expanding personal consumption. The relatively high personal savings rate suggests that there could be pent-up consumer demand to put that money to work. This week’s chart highlights total consumer credit outstanding, which has declined considerably since its pre-pandemic peak at the end of February. The decline in personal balance sheet leverage suggests that American households can access credit as needed or desired. This data is not very timely as June 30 is the most recent report, but it does suggest that the consumer is not as distressed as in previous recoveries.

The labor market continues to be the most restraining issue facing the economy — 14.8 million continuing jobless claims with initial claims amounting to 1.1 million this past week. But, the Bureau of Labor Statistics reported July payroll jobs expanded in 40 states, declined in one and were essentially flat in the remaining nine. We do need a broader and more inclusive jobs recovery because, as the BLS reports, the large increase in average hourly earnings is not good news — It reflects lower-paid workers being pushed out of the work force due to COVID-19 related business suspensions and closures. Strengthening trends in housing and manufacturing should spur further job growth and help restore this disenfranchised segment of the workforce. [Chart courtesy US Federal Reserve, Bloomberg LP (c) 2020]

Over the last several months we have cited several factors that, in our view, explain why the US stock market indices have been rising and may continue to do so. The most significant contributors are measures being undertaken by the US Federal Reserve and Federal government to support the labor market. The US consumer has been responding by increasing consumption, and so we see core components of the US economy like auto purchases and manufacturing rebounding. The official unemployment rate is still terribly high, measuring 10.2% in July, but that is a significant improvement over 11.1% in June.

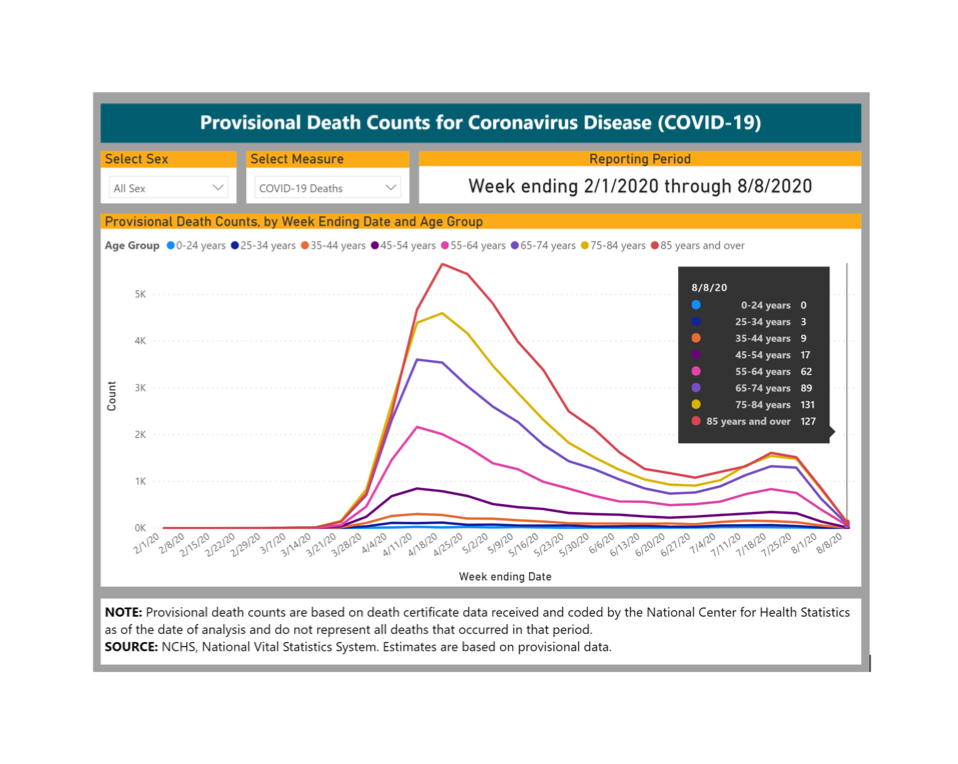

Pandemic-related government-mandated lockdowns are being lifted (although in some areas of the country those being reinstituted) and economic trends should continue to improve as people return to work and to consumption. Critically, there are encouraging signs related to COVID-19. According to the National Center for Health Statistics (part of the CDC), weekly total provisional deaths as of August 8th registered 438, lower than the pre-surge figure registered on March 21st. These totals are significantly lower than figures cited by media outlets and Johns Hopkins University, a consequence of how deaths are verified and reported, but most importantly we are seeing improving trends regardless of methodology, and that is a relief. Very well known yet still necessary to point out, this week’s chart demonstrates the concentration of fatalities for those age 55 and older, showing the terrible risk to and impact on the elderly. But, by contrast, the low concentration and declining trend among the young may alleviate concerns about the upcoming school year and broadening re-openings across the country.

WCM has made some changes to our monthly newsletter to make it more engaging and useful for our readers. First, we have moved our interpretive analysis of the month gone by to the front and expanded it. We follow that with our current portfolio positioning and what we see as the capstone risks to our stance. Lastly, we close with a performance survey of capital markets for the prior month, calling out what we see as the most consequential returns which played into both our thinking and our results.

As always, you can find our latest newsletter in the Library, along with an archive of prior newsletters. Thank you for reading!

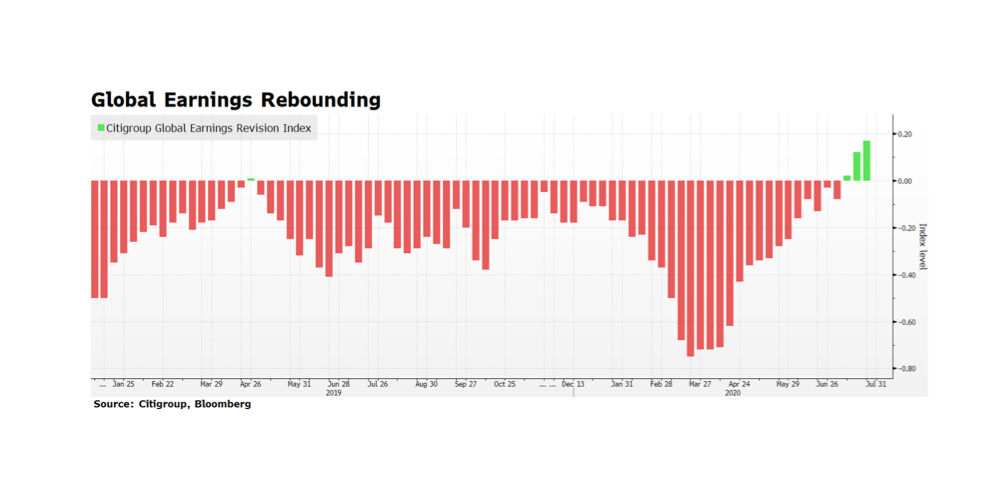

Over the past few weeks, corporate earnings across the globe have been showing signs of recovery. Citigroup’s Global Earnings Revision Index has been climbing for three weeks in a row, encouraging given the economic challenges facing the world. While this trend is positive, its path will be unpredictable due to COVID-19 related shut down and re-openings in several key economies. The recovery in corporate earnings, if it persists, could alleviate the tragic stress in labor markets and help reinvigorate economic activity heading into 2021. Fiscal support is building momentum with the European Union’s 750 billion Euro stimulus plan (discussed last week) and the anticipated fourth phase of US stimulus. It does remain to be seen if the enormous amount of spending, both fiscal and monetary, will have a lasting impact.

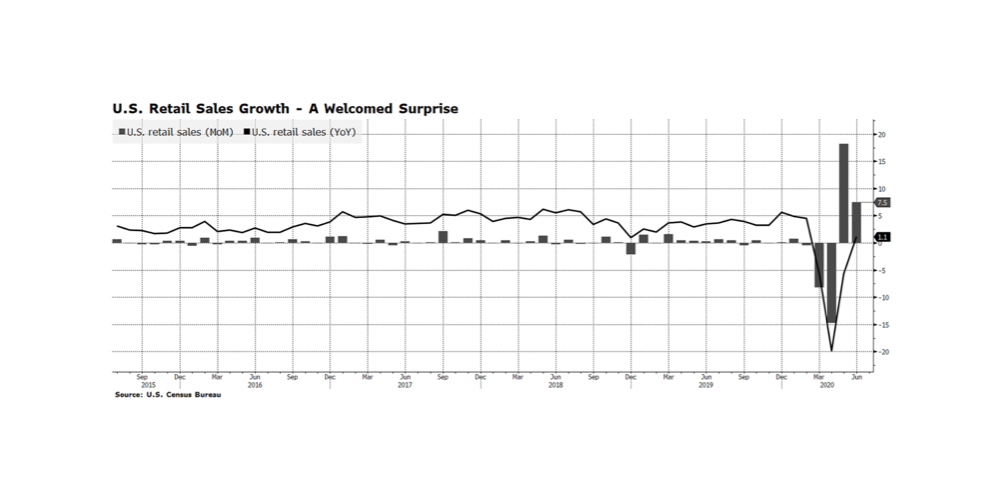

On Thursday, July 16th, the US Census Bureau released Retail Sales figures and month-over-month growth registered a nice surprise — 7.5%, well above the consensus estimate of 5.5%. The prior month’s figures were also revised upward. We see this as an obvious reflection of the reopening of the US economy and pent up demand. But, we don’t read much into the positive monthly gain versus the consensus estimate because economists have never had to forecast under conditions that can be considered “lock-down uncertainty”. What we do find encouraging and more interesting is that the reported annual growth rate was 1.1%. At this time last year the US economy was on firm footing, and yet Retail Sales are modestly above those levels today. While the trajectory of sales growth is a relief, we would not be surprised to see some sluggishness emerge as we collectively digest the flurry of initial purchasing pre-quarantine and new virus spikes elicit further lockdown measures. [chart courtesy US Census Bureau, Bloomberg LP (c) 2020]

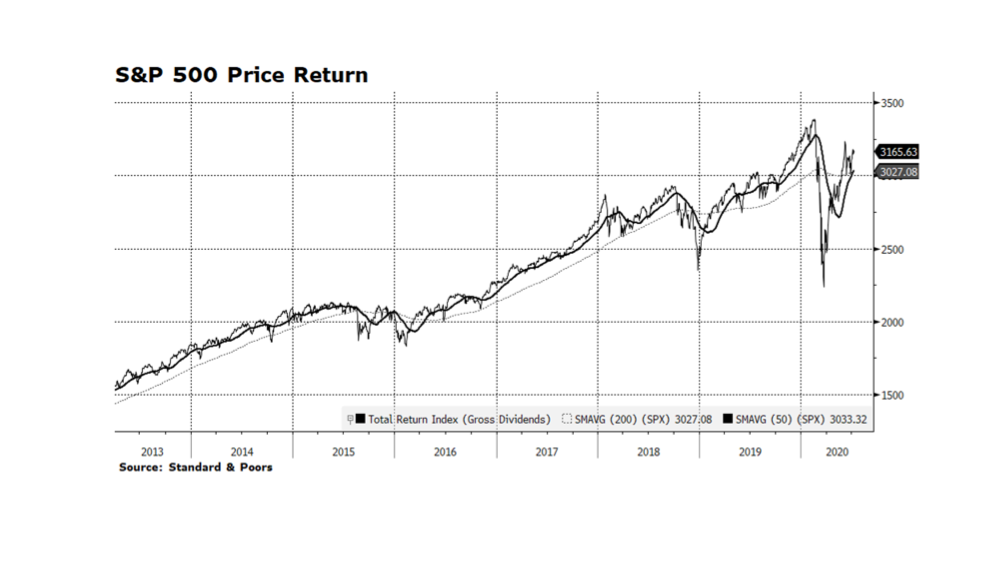

Equities in the US have been rallying since late March. The total return of the S&P 500 is 41.7% from the crisis trough on March 23 through July 9. The recovery in stocks has been among the swiftest in history and has caught many market participants underinvested during this uncertain pandemic period. Even with tremendous stress in the labor market, the overall economy and current corporate earnings, the S&P 500 price level has produced a widely followed bullish technical pattern know as a “golden cross” after Thursday’s close. This formation occurs when two key trend lines, the 50-day and 200-day moving averages, intersect while trending upwards. Generally, this condition needs to be supported by other factors, such as the powerful fiscal and monetary stimulus which we have been highlighting for the past several months, as the main reason markets have been rebounding. Another positive development is influential investment research organizations have begun to increase corporate earnings expectations for 2021. There are still well-known risks including the ebb and flow of the global pandemic and China-related tensions with the rest of the world. We expect volatility in the capital markets emanating from these and other factors, but equities, particularly in the US, will grind higher. Chart courtesy Bloomberg LP and Standard & Poors (c) 2020.

We are very proud to announce that we are joining forces with HealRWorld, Angels.Inc., and the SDG Impact Fund as the lead advisor for two new donor advised funds (DAF). Each DAF is driven by a specific mission to direct capital in pursuit of the United Nations Sustainable Development Goals. The first DAF, the HealRWorld SDG Impact Fund, is focused on improving access to financial resources to fuel business and capital formation and catalyze growth for women- and minority-led small businesses. According to MPAC Solutions, a scant 1.3% of $70 Trillion of institutional capital is allocated to women and diverse management teams. The HealRWorld fund is raising capital through the charitable structure to make mission- and program-related investments in these small businesses that demonstrate strong ESG attributes and an orientation toward attaining one or more of the SDG targets. HealRWorld’s proprietary data and analysis has demonstrated that small businesses with strong ESG attributes are up to 3X more credit worthy than the typical small business, making them both good businesses and good risks.

The fund will also make strategic investments in community- and small business-oriented targets, both through lending and taking equity stakes, in order to further align investment with mission and amplify the potential outcomes from capital raised in the DAF, as well as bring coinvestment capital to the table to multiply the available resources for these businesses.

Equally exciting is the Angels.Inc SDG Impact Fund. The Angels.Inc fund is focused on funding media projects and ventures that are contributing vastly to innovation for the betterment of society and our future as well as contributing to our well-being, mental health and amplifying the positive messages and goals of the United Nations Sustainable Development Goals (SDGs). The investment mandate for the Angels.Inc. fund is more expansive than the HealRWorld fund, committing to investing in the same small businesses, but will also invest in and fund media-related targets consistent with Angels.Inc’s “Media For Good” mandate.

For more information or to make a commitment to these amazing charitable efforts geared at empowering and ennobling business and media to lift up and serve everyone equally and inclusively, please visit our Philanthropic Services page, email the Funds at [email protected], email us at [email protected], or call us at 866-894-5332.

Every member of an eco-system, from vegetation to predator species, plays an integral role in the sustainability of that system. When one player is removed from the hierarchy, whether by result of climate change, pollution, human development, or natural occurrences, the effects are cascading. An often overlooked and yet essential vulnerable group of species is pollinators. Although bees and fruit bats are not the poster children for endangered species like tigers and elephants, their role in pollination facilitates an ecological process critical for the reproduction of wild flora and agricultural crops.

(c) 2020 P. Sorgi

According to the U.S. Department of Agriculture, more than 150 crop species in the United States, including blueberries, tomatoes, apples, bananas, and peaches, rely on pollinators annually. Alfalfa and other grain crops necessary to sustain livestock also rely upon pollination. Furthermore, more than half of the world’s diet of fats and oils are produced from animal-pollinated plants (sunflowers, almonds, canola, avocados). Honeybees alone are responsible for pollinating $15 billion in crops for the U.S. economy each year (Main, 2020). Plainly speaking, without pollinators, the globe’s future food security collapses.

Without pollinators, you can drop the dinner table conversation because there quite literally won’t be a dinner

So, where does the issue reside? According to Penn State University’s Center for Pollinator Research, since 2006, the honeybee population in the United States has declined 30-42 percent each year largely due to the impacts of climate change, habitat loss, and toxic pesticide use. Of the 65 species of flying foxes (fruit bats), 31 are threatened with global extinction (Vincenot, 2017). Protecting species of pollinators is not just the “right thing” to do; it’s compulsory for human existence.

As managers of sustainable and responsible investment portfolios, our passion lies not only in providing ethically sourced returns for our clients, but in supporting positive impact-driven organizations. Conscious investing is achieved through avoidance of institutions that harm ecosystems, in conjunction with focus on institutions that provide regenerative and resourceful solutions. [artwork (c) 2020 P. Sorgi]