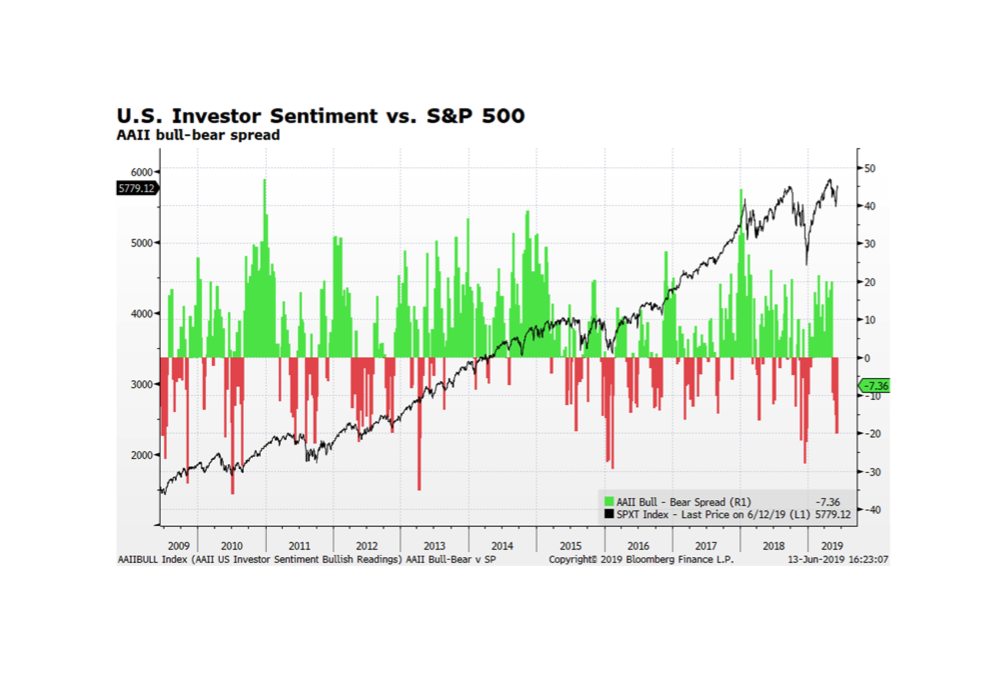

Investor sentiment in the US is bearish as the American Association of Individual Investors’ net bull minus bear spread currently registered its third negative reading and now stands at -7.36. That is the bad news. But, this contrarian metric can signal market upward and downward shifts when registering positive or negative extremes. The gauge registered -20 last week, so the most recent figure, although still negative, is an improvement and could provide psychological support to carry further gains in US stocks.

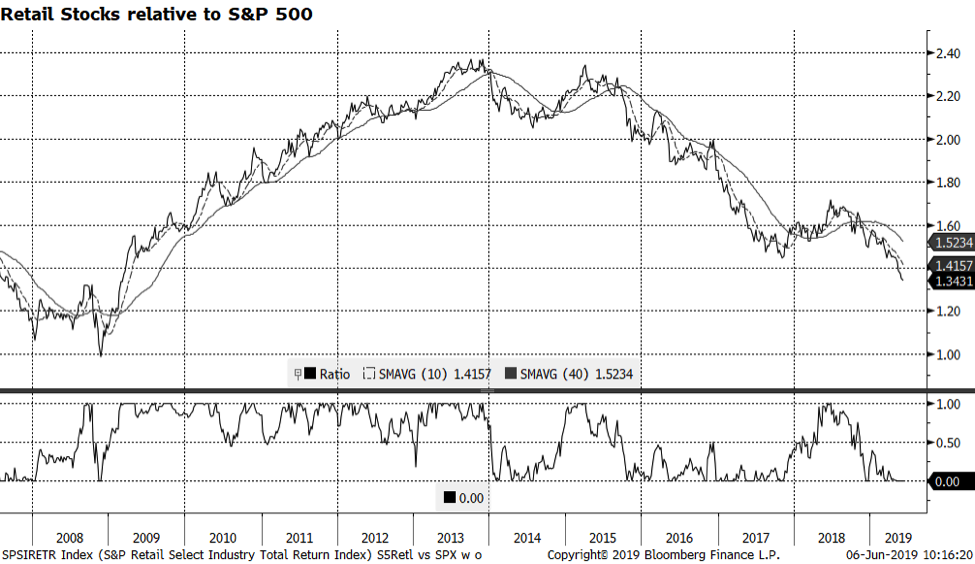

The American consumer remains fairly strong, and yet the retail sector is not keeping pace with the broader market. What is wrong with retail then? Our view, which is consistent with those of portfolio managers that we follow and respect, is that the US is simply “over-retailed”. There are too many ways and places to buy the exact same things. Yes we are seeing structural changes as we lurch forward (backward?) to the good old days of catalog shopping and home delivery, just in the shiny wrapper of smart phone apps and curated boxes. But, the old channels are suffering but have not gone away. Yet. There are zombie brands that should have winked out of existence years ago that trudge along on fumes, debt or hedge fund and private investment. We are still surrounded by big boxes, shopping centers, strip malls, mega-malls, outlet malls and Main Street, but what we can buy across all channels, physical and virtual, is homogeneous. Experiences are driving consumer channel behavior. Service, price and convenience are the factors that will force the inevitable and messy shakeout. Until there is some real carnage and consolidation, expect retail to be a challenging place to outperform.

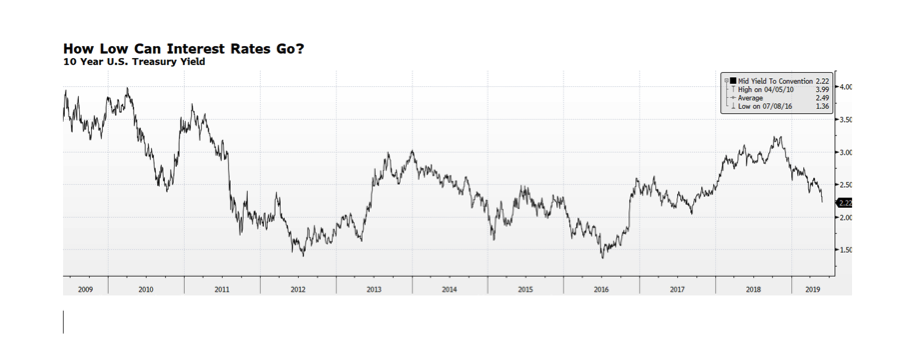

The yield on the 10-year US Treasury has fallen to 2.22% (as of May 29th) which is 100 basis points from the recent high reached on November 8, 2018. The rapid decline in rates, 29.8% from last November’s levels, has many investors unnerved as a portion of the yield curve is inverted. That historically has signaled oncoming recessions. Interest rates could fall further from here. Over the past decade, there have been at least seven distinct periods where yields have fallen, averaging over 39% from peak-to-trough. The duration of those periods averaged 7.6 months while the current downtrend has lasted six months, 11 days and counting. There are several reasons why rates could continue to fall, ranging from the ongoing and unpredictable effects of the US-China trade negotiations, political disfunction in the EU and Great Britain, the lack of inflationary pressures globally and negative interest rates for comparable government bonds in Germany and Japan. The risk for investors chasing this treasury rally is that any escalation in yields from these low levels would result in material loss of principal. [chart courtesy Bloomberg LP (c) 2019]

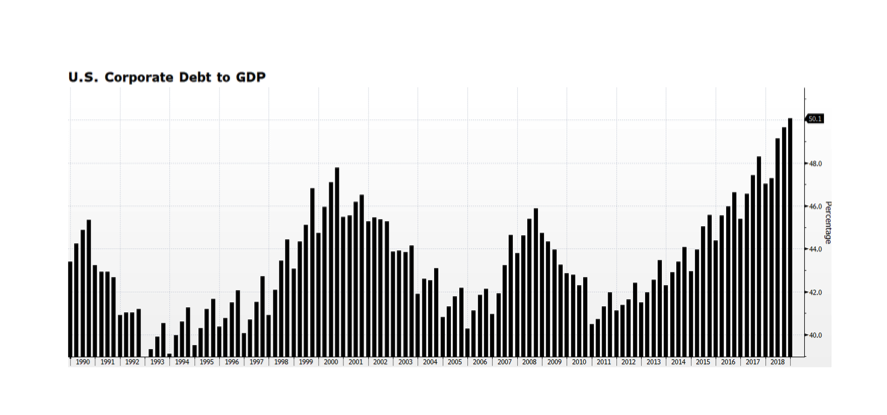

Monday’s remarks by Jerome Powell, Chairman of the US Federal Reserve, raised some eyebrows in financial circles. He stated “Business debt has clearly reached a level that should give businesses and investors reason to pause and reflect” and “Another sharp increase… could increase vulnerabilities appreciably”. These comments prompted some investors to draw comparisons to the mortgage crisis. The chart below shows US corporate debt to GDP levels, currently at a 30-year high of 50.1% (vertical axis), and it is alarming. Not only does the current reading exceed the Financial Crisis but the measure also exceeds readings reached during the debt-fueled technology bubble era. One major difference today is that during both previous crises, interest rates (yield-to-worst according to the Bloomberg Barclays US Corporate Debt Index) were near or above 8% whereas now rates stand at 3.6%. Powell did qualify his comments by adding that debt servicing costs remain low and debt growth is in line with GDP growth. Cold comfort unless rates remain structurally lower for longer.

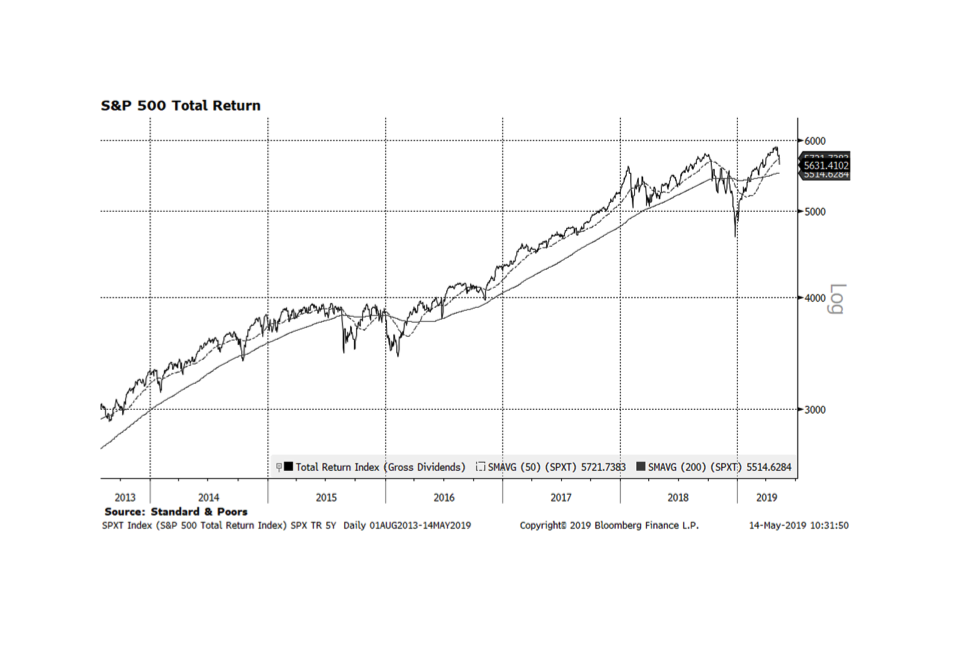

US stock markets have continued to be roiled by ongoing US-China trade negotiations. Departing Washington DC last Friday, Beijing issued a strong statement challenging US demands for fairer trade. The core issue for the Chinese is that the US is forcing the Chinese to change their laws regarding intellectual property protection, dispute resolution enforcement, and mandatory joint ventures, among other issues. That is seen as an affront to Chinese sovereignty. Beijing needs to “save face”, avoiding being seen as a weakened nation from a domestic perspective and just as importantly throughout the region. To form a trade agreement with the US, China’s lead negotiator Liu He will have to concede on these points which will then form the template for other major trading partners such as Europe to follow. Beijing probably realizes that, by giving ground to the US now, it is only a matter of time before their decades-long trading advantages evaporate. While this major global event plays out, we expect more volatility and would not be surprised to see US stocks test or even trade through their long-term trends as depicted by this week’s S&P 500 Total Return chart.

The on again off again trade spat with China seems to be peaking this week. Tonight is when the new tariff regime is supposed to go into effect if the two sides do not come to a different accommodation. There is of course some question of whether President Trump (or Xi) will blink and business can continue as usual. If we learned anything from the government shutdown over the holidays, it is that DJT will not hesitate to do a Thelma & Louise and take us collectively over the cliff. In his bare-knuckles negotiating style, the other side has to believe there is no bridge too far to get what you want.

And, there is a very strong case that has been made over decades that China needs to bend. They have benefited from overly generous policy for decades now that allowed them to build their economy while Western markets used them as a cheap outsourcing factory. Part of the price paid was a systematic forfeiture of intellectual property and inability to truly participate in their market. The benefit was, in two words, cheap stuff. With low wages, few environmental controls, and a myriad of other reasonable and questionable policies and practices, we enjoyed a tremendous arbitrage between their ability to make and our ability to consume that gave us everything from full shelves at dollar stores to affordable smart phones and other consumer electronics.

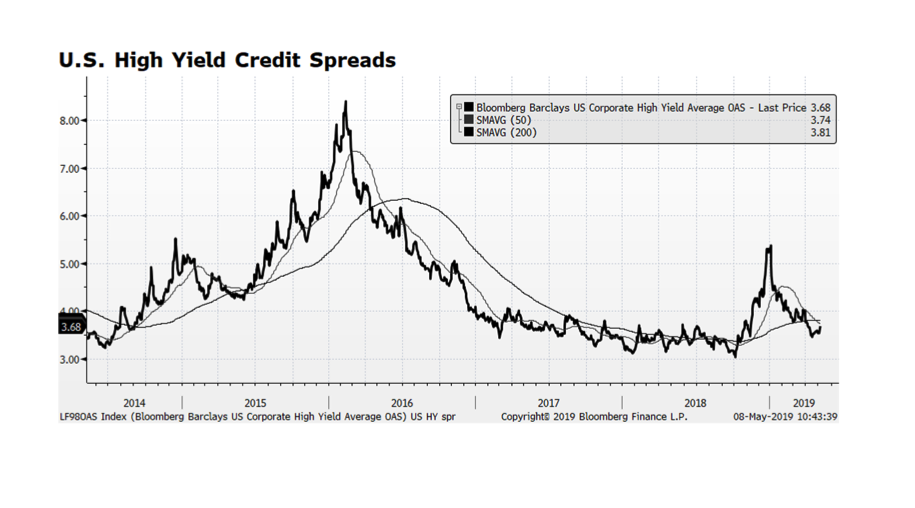

Interest rate spreads in

the US High Yield bond market have risen recently after narrowing some 130

basis points since the beginning of the year.

While that is a concern, we point out that current readings are still below

trend. Comments from Pres. Trump over

the weekend regarding tariff increases in trade negotiations with China have

rattled stock and credit markets around the world and undoubtedly contributed

to the near-term widening of US High Yield spreads. How these negotiations play out towards the

end of the week are critical for the capital markets. Key components of the

earlier discussions – intellectual property protection, dispute resolution enforcement

and freer market access – may be in jeopardy or be diluted. That could lead to

economic disruption and derail the recovery in risk asset classes we have

experienced so far this year.

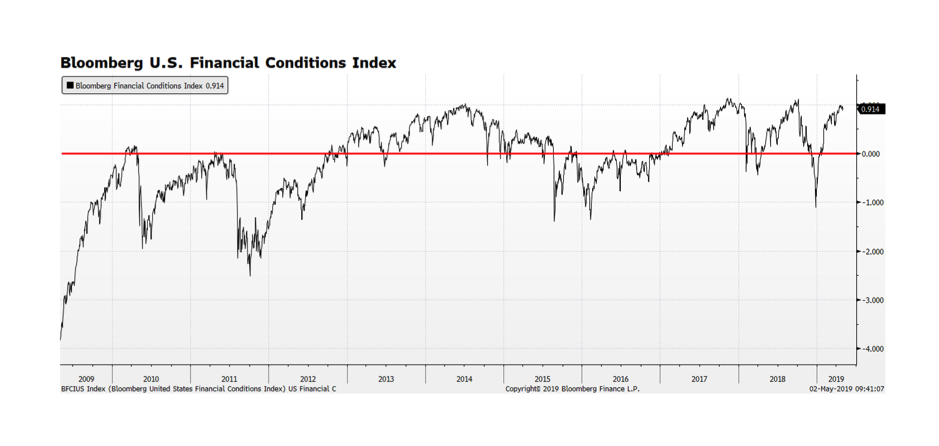

Bloomberg maintains a series of global and regional financial conditions indices that combine several key fixed income and equity market metrics such as interest rate spreads and volatility. Taken together, this data gives an indication of how benign or strained conditions are in the capital markets. Currently, the reading in the US is positive, indicating a benign environment for risk asset classes. It is important to recognize this indicator can maintain long periods of positive or negative readings but when it begins to move in a downward direction capital markets become stressed. US financial conditions could continue to remain in a positive state due to favorable economic trends — low inflation, accommodative monetary policy, strong productivity gains, high labor participation and robust GDP growth.

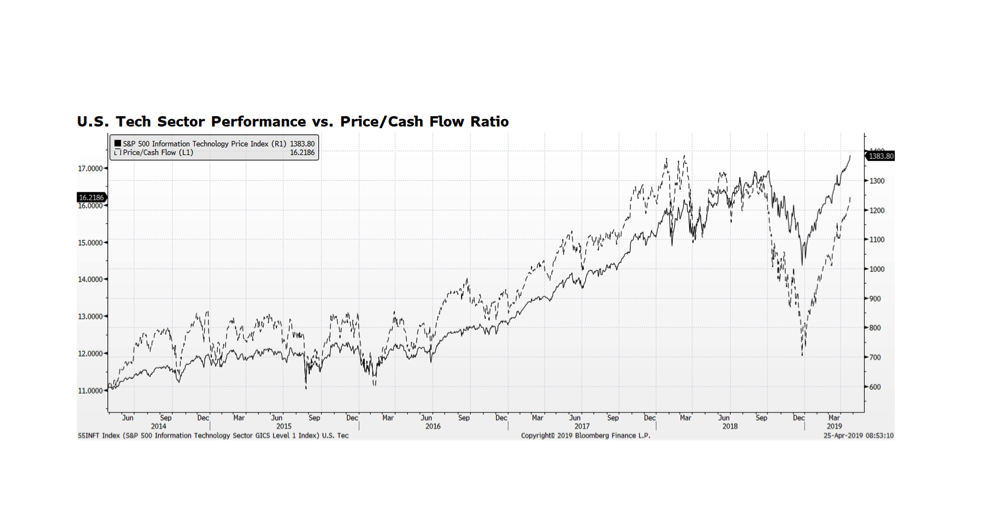

A little off-schedule so

we’ll call it the Chart of the Moment. Based on Standard & Poor’s indices,

the rebound in US technology stocks since the beginning of the year is an

impressive 27.8% while the overall equity market has advanced 17.5% through

April 24th. US technology

companies play a critical role in the American economy and the sector is the

largest in the US equity market based on capitalization. Further gains of US

equities overall largely depend on tech sector performance and valuation

readings are approaching historically high levels. We show the technology

sector along with its price-to-cash flow (P/CF) valuation metric. The current P/CF is 16.2 which is below last

March’s five-year high of 17.6 but still in an area where the sector has

struggled. We are currently in the midst

of the US earnings season, and if technology companies can continue to deliver

strong earnings and cash flow, share prices should advance further. (all data

citations as of April 24, 2019)

The Eurozone has faced several roadblocks to growth since the Financial Crisis ranging from the debt crises in Italy and Greece, to the uncertainty related to Brexit to stubbornly sluggish economic growth. We have been concerned that economic conditions on the Continent would strain corporate performance and therefore we have not been fully committed to Eurozone equities for quite some time even though the region has favorable valuations compared to global peers. Now there may be positive trends developing. This week’s chart shows Citigroup’s Earnings Revision Indices for Continental Europe and the Globe. The latest reading for Europe was flat while the World registered -0.12. Both indices appear to be trending towards positive revisions which could provide a key underpinning for further gains in global equity markets. If positive developments continue in the European corporate sector, investors may rotate funds into the region.