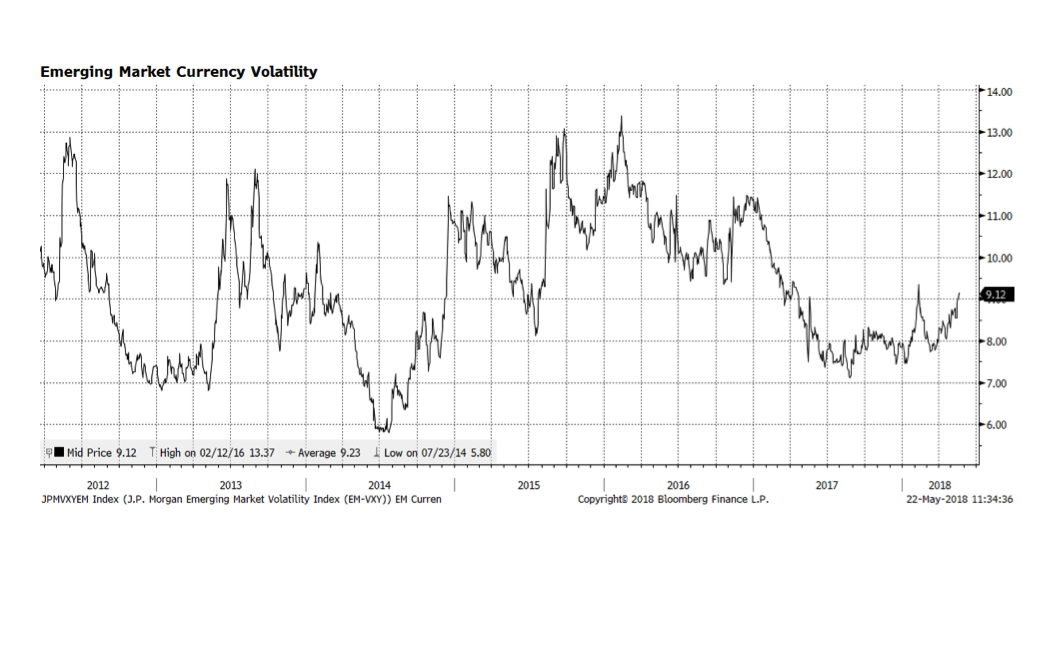

Several currencies in developing economies have been weakening against the US dollar and not surprisingly, volatility, depicted on the chart below, has been rising. Part of the fallout is related to US dollar strength against the Euro, Japanese Yen and British Pound but rising interest rates in the US are also a significant influence. External dollar-denominated debt issued by emerging economies in recent years has risen and repayment could be challenging if the dollar continues to strengthen. This warrants monitoring. We continue to have no emerging market debt exposure at this time.