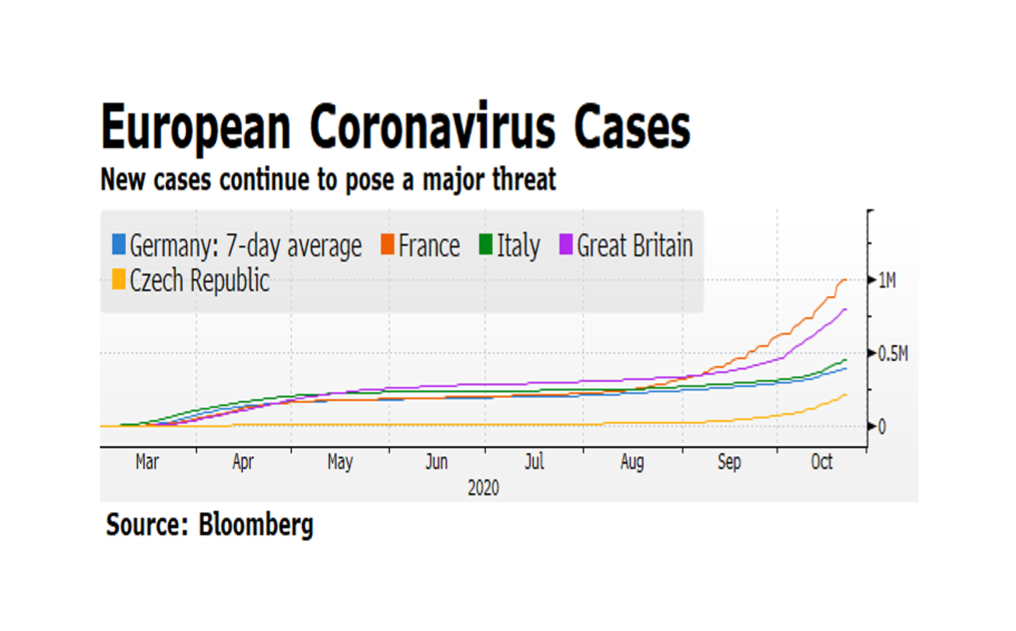

Over the past decade or more, Europe has endured several painful crises spanning Euro-related stresses to the recent Brexit uncertainty. The common thread retarding recoveries from these epochal events has been the lack of coordinated policy response, in particular fiscal stimulus. The European Union, now with the UK removed, simply does not have the strength to influence its member states to expand fiscal spending that would benefit the region beyond each country’s own national borders. Now the global Coronavirus pandemic is accelerating to frightening levels across Europe as evidenced by case momentum. The imprint on European stock prices is telling. From the onset of the pandemic, the broad-based EuroStoxx 600 is over 8% lower in US dollar terms and has been range trading since early June. By contrast, The S&P 500 is flirting with all-time highs. We believe the difference is that, while Europe has generally been more aggressive in the public health response to the pandemic, the overwhelming US fiscal and monetary response carries the day as compared to the apparent EU policy vacuum.

Wildfire has had profound implications both for and because of climate change, for ecosystems, for communities, and for public health and safety. Wildfire has also had major economic consequences. Loss of housing, loss of commercial space, loss of public infrastructure, loss of crops, and loss of tourist revenue all add up to tens of billions of dollars a year just in the United States. The risk of wildfire conspiring with a lack of adequate governance and safety practices led to devastating financial losses and convictions on 84 counts of manslaughter for one of the largest utilities in the country. This week’s chart is from Munich Re and NatCatSERVICE by way of the Insurance Information Institute showing wildfire losses over the last decade (expressed in millions). Note that the spike in 2017 was so significant that the data from prior years is swamped by scale. While 2019 appears to have been a more modest loss year on par with earlier in the decade, according to the National Interagency Fire Center (nifc.gov) as of October 19th this year nearly twice as many acres have burned as by the 19th of last year, on pace with 2018 and 2019. The tale has yet to be written but that would suggest another likely spike in insured and uninsured losses. Economic loss is as much about the incidence of wildfire as it is the private encroachment on wild spaces. People increasingly work, farm and live in vulnerable forested and grassed spaces based on a history of relative fire scarcity that no longer exists. Without addressing both the climate systems issues to mitigate fire risk, and the resiliency of communities and businesses in the face of more frequent and prevalent fire, economic losses will continue to climb.

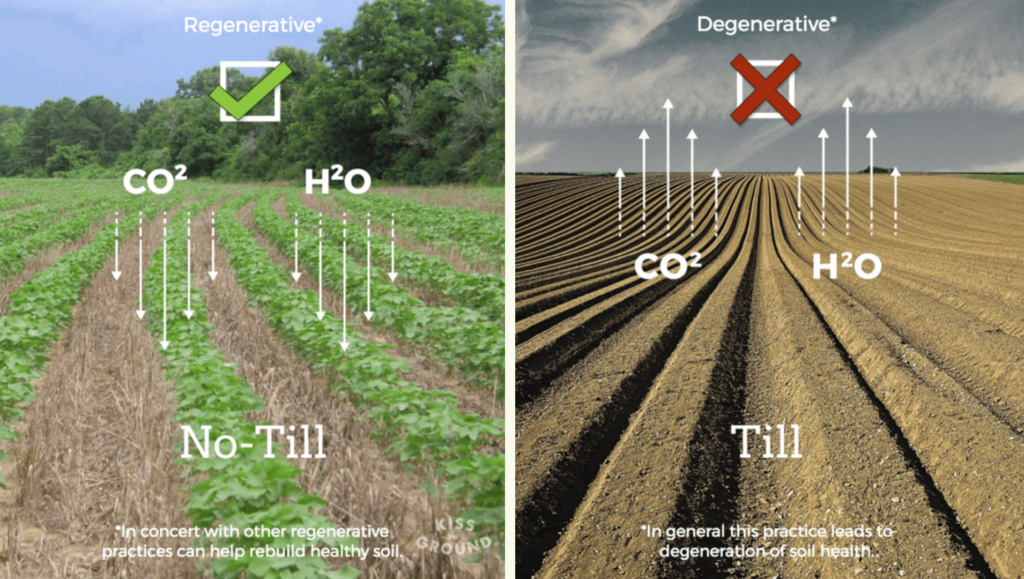

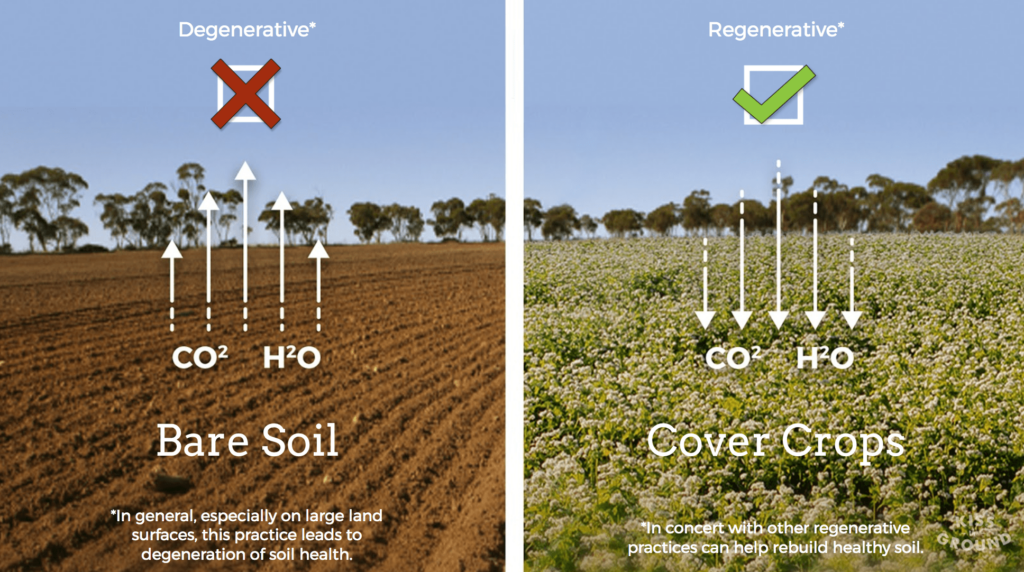

The popular, if you can call it that, view of rising carbon levels in the atmosphere is that the carbon problem is primarily an industrial problem. Oil, coal, and gas extraction and refining, power generation, factories, automobiles, chemicals, concrete, do all contribute to atmospheric CO2, and the trajectory of climate consequences tracks well with the Industrial Revolution. But what is far less well understood, but may be of much greater consequence, is global soil health. Modern agriculture, driven by feed lots, monocultures, tilling, chemical pesticides, and off-season bare soil has been systematically eliminating healthy soil as a global carbon sink. From an economic perspective what is really stunning is that these practices actually don’t result in more profit and productivity per acre for farmers. This week’s images are from Kiss the Ground, an initiative to help the world transition (back) to regenerative agriculture, which is better for both planet and profit. Become a soil advocate at www.kisstheground.com, and check out the documentary now streaming on Netflix. #kissthegroundmovie

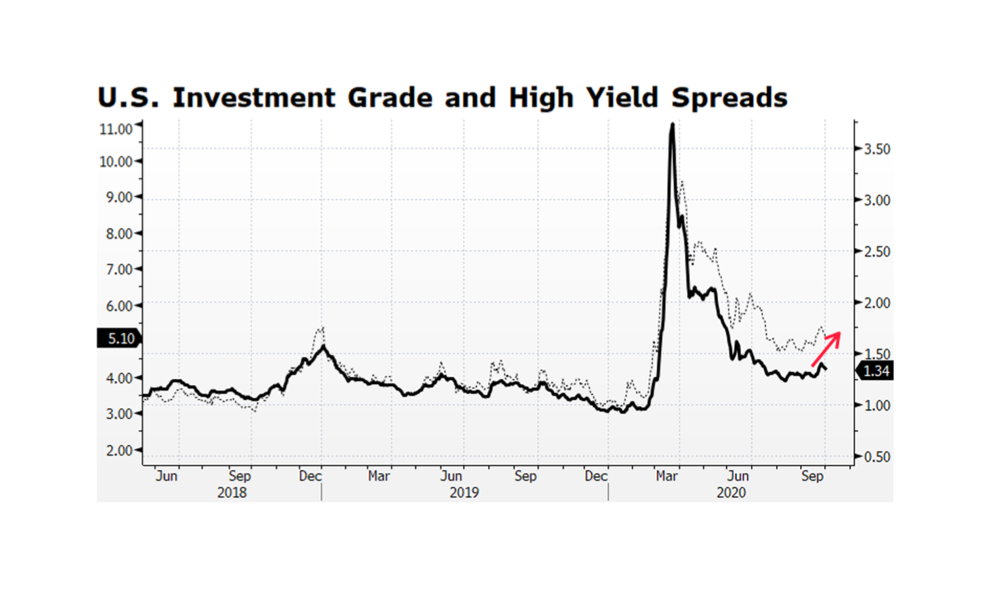

Over the past several weeks, credit spreads in US Investment Grade and High Yield bonds have risen while US equity prices hover near key support levels established since the S&P 500 and Nasdaq Composite indexes posted record highs in early September. Some consolidation in equities can be justified given the rapid recovery from the pandemic-induced lows reached in late March. The bond market appears to be sensing heightened risk. Credit spreads fell a considerable amount since the late-March spike but remain elevated compared to pre-pandemic levels and are on the rise even considering the modest tightening this past week. The yield on the 10-year US Treasury has been relatively stable since the beginning of September, fluctuating 5-10 basis points, and the US Federal Reserve remains in hyper-accommodative mode implying that the rising price of money for US corporate creditors is the main driver of widening spreads. This trend suggests that there may be further volatility ahead for US corporate securities. [chart courtesy Bloomberg LP (c) 2020]

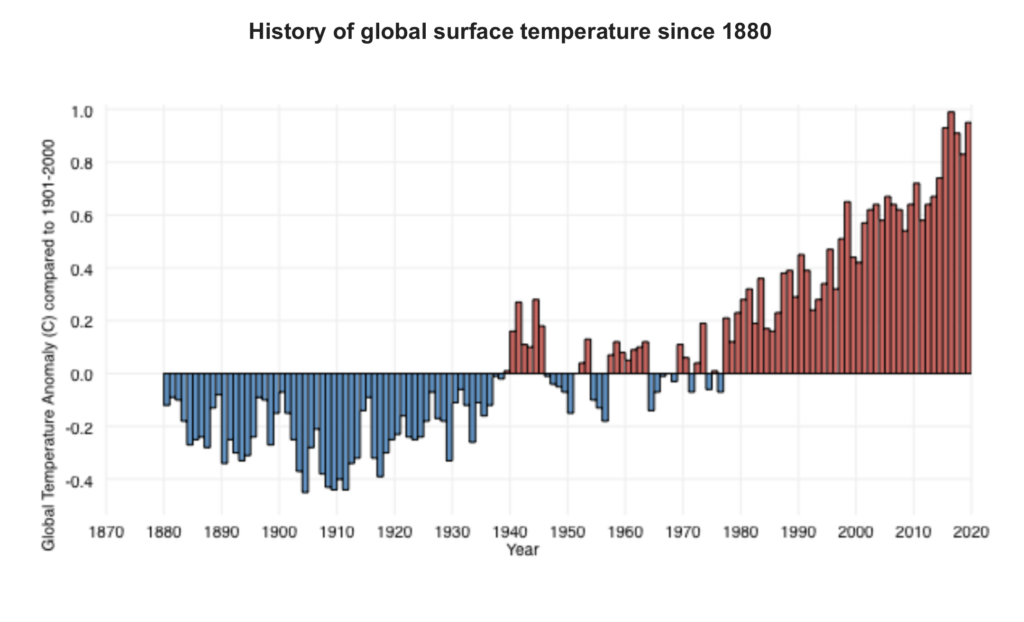

As we close out Climate Week, we need to check in on global temperature. It is climbing. Climate scientists, environmental advocates, legislators, etc. have taken to talking about “climate change” because there has been so much rhetorical pushback about “global warming”. But as the data shows, global average annual temperatures are demonstrably higher as compared to the long-term average over the last century, and decisively trending higher from the pre-Industrial period. In finance we use charts that look like this to argue the benefits of investing in stocks. Trend followers would consider this a definitive and stable factor. Climate change is the outcome and global warming is the driving factor. From a capital markets point of view a professional investor would be derelict for ignoring this data. Scientists still believe mean reversion is possible if we withdraw greenhouse gases (GHGs) from the system. Prudent investment involves deploying capital for mitigation – the reduction in GHGs to reduce climate volatility – and resilience – improving infrastructure, businesses and communities to be able to handle or ideally prevent climate-related damage. [chart courtesy NOAA, August 2020 – https://www.climate.gov/news-features/understanding-climate/climate-change-global-temperature]

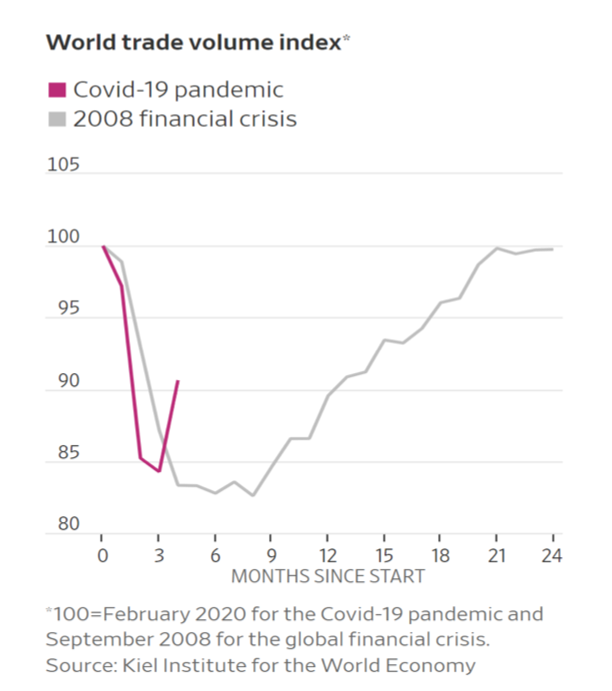

This week’s chart appeared in the Wall Street Journal via Germany’s Kiel Institute for the World Economy and shows the rapid rebound in global trade after the pandemic-induced economic stall. As the Journal points out, World trade volume has regained half of the volume lost since the COVID-19 outbreak in three months whereas it took nearly 12 months for world trade to regain a similar drop in volume in the aftermath of the global financial crisis. While the rebound is not consistent across the globe, it is an encouraging sign that commerce is returning to normal.

What we find notable is the speed of the recovery in trade volume and consistency with our comments last week regarding the fast pace of US jobs re-creation. The causal nature of this recession was highly unusual, near universal global government-led economic lock-down, so it is not all that surprising that the recovery could be quicker than normal. Several factors could disrupt the recovery including a potential second wave of viral infections, lack of an effective vaccine or therapeutics, and ongoing trade tensions. But, improving macroeconomic trends are welcomed worldwide.

“Global warming: the long-term heating of Earth’s climate system… due to human activities, primarily the burning of fossil fuels, which increases heat-trapping greenhouse gas levels in Earth’s atmosphere,” (Shaftel, 2020). The term coined decades ago has gained momentum in not only scientific communities and environmental organizations, but political campaigns and industry corporate governance policies around the globe. From polar ice melting and sea levels rising to extreme weather events, our changing climate has far reaching and compounding effects on the environment and ecosystems, our economies and industries, and our global food supply. One of the direct effects of climate change and global warming is ocean acidification.

To examine the process of ocean acidification and its impacts on human life, recall an adolescent science lesson on pH and water chemistry. The pH scale runs from 0-14, with 7 being neutral. Higher than 7 represents a basic or “alkaline” pH and lower than 7 represents an acidic concentration. For reference, household vinegar, an acidic liquid, has an average pH of 2.5, while tap water has an average pH of 7.5. The ocean’s current pH is approximately 8.1, which is basic (NOAA, 2020). How does the ocean’s pH tie into global warming and climate change?

The ocean naturally absorbs roughly 30% of the carbon dioxide that is released into the atmosphere. When seawater and carbon dioxide combine, carbonic acid is produced, lowering the pH of the ocean and increasing the acidity. As levels of carbon dioxide increase due to human activity (burning of fossil fuels, land-use change and deforestation, agricultural industries) the amount of CO2 absorbed by the ocean also increases. Plainly speaking, the more CO2 we produce and release into the atmosphere, the more acidic our oceans become. Since the Industrial Revolution in the 1700’s, increases in CO2 have resulted in a 30% increase in ocean acidity (NOAA, 2020). This present acidification process is occurring ten times faster than any previous changes over the last 300 million years (IUCN, 2017). The rapid acceleration of CO2 production significantly jeopardizes the ability of ecosystems to effectively adapt to the changes in ocean chemistry.

Increased ocean acidity especially affects organisms with calcium carbonate shells or skeletons including shellfish like coral, oysters, crab, and lobster. A recent study performed by the National Oceanic and Atmospheric Administration on the pteropod, a small sea snail integral to the ocean food chain, showed that the levels of ocean pH projected for year 2100 dissolve the organism’s shell within just 45 days. Furthermore, researchers have already discovered severe shell dissolution in pteropods naturally found in the Southern (Antarctic) Ocean, indicating the process’ rapid progression (NOAA, 2020). The pteropod snail is a major food source affecting members of the food chain from krill and fish to whales and seals. When we consider how each organism is interconnected in the food web, the loss of one species creates a cascading effect.

Unfortunately, the consequences do not stop there. Increased acidity has also been linked to a disturbance in scent transmission, inhibiting species from detecting predators and locating suitable habitats (NOAA, 2020). Acidification has also been observed to affect sound transmission, reducing sound absorption and increasing the ocean’s ambient noise (OAN). Increases in OAN can impair marine animals’ hearing and communication, increase stress and lower their immune systems, and even cause brain hemorrhaging or death in severe cases (Gazioğlu, 2015).

High Level Impacts

In 2018, the global fishing and seafood sector represented a USD 164 billion international trade industry employing 59.5 million people. 88% of the 179 billion tonnes of total fish produced in 2018 was for direct human consumption. Fish and fish products supply approximately 3.3 billion people with nearly 20 percent of their average per capita intake of animal protein. Furthermore, seafood provides many crucial nutrients to the human diet including long chain Omega-3 fats, iodine, vitamin D, iron, calcium, zinc, and other minerals. With key species like the pteropod in jeopardy, the entire seafood industry risks significant threat, exacerbating global hunger and malnutrition (FOA, 2020). Dying coral systems lack the ability to effectively buffer coastal communities from storm waves and erosion, and leave those communities to suffer consequences to tourism and commercial business (IUCN, 2017). Profits, careers, economies, biodiversity, ecosystem structure, shoreline integrity, and global food supply are all threatened if ocean acidification continues to accelerate due to increased CO2 production.

As managers of sustainable and responsible investment portfolios, our passion lies not only in providing ethically sourced returns for our clients, but in supporting positive impact-driven companies and communities. Conscious investing is achieved through selective avoidance of institutions that harm ecosystems or using the allocation of capital as a lever to change those institutions, in conjunction with focusing on institutions that provide regenerative and resourceful solutions to humanities’ needs.

Gazioğlu, C., Müftüoğlu, A. E., Demir, V., Aksu, A., & Okutan, V. (2015). Connection between Ocean Acidification and Sound Propagation. International Journal of Environment and Geoinformatics, 2(2), 16–26. https://doi.org/10.30897/ijegeo.303538

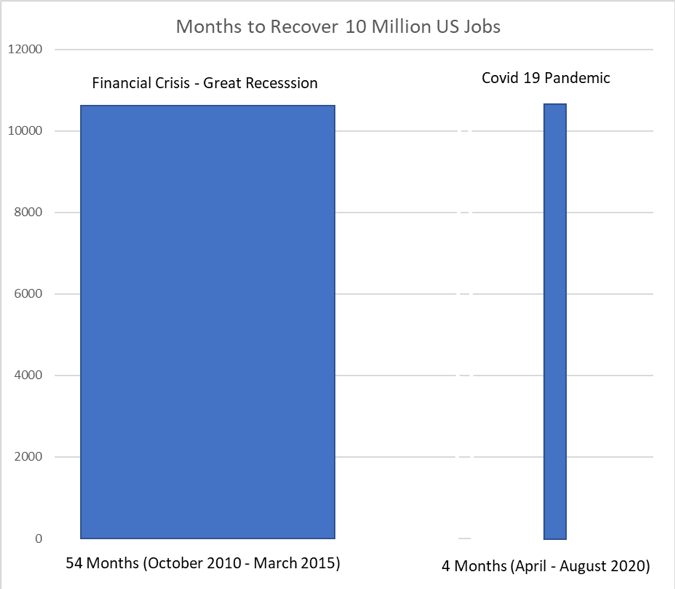

August’s labor market statistics were encouraging and suggest that the US economic recovery is far from normal. According to the BLS, Nonfarm Payrolls expanded 1.37 million in August, slightly above expectations, and the unemployment rate dropped by more than expected to 8.4% versus consensus expectations of 9.8%. While the number of unemployed dropped by 2.8 million, there are still 13.6 million Americans out of a job, which is 7.8 million more than in February. The nature of the recession, which appears to be largely behind us, is like none ever experienced because it was government induced nearly worldwide. Governments across the globe intentionally suppressed economic activity rather than act in their normal supportive role. Recessions are often caused by structural imbalances such as excess leverage in the financial sector, over-accommodative monetary policy causing hyper-extended stock market valuations, overvalued currencies and commodity price shocks. These types of imbalances did not exist in the US for the most part prior to the pandemic and that may have set the conditions for a faster recovery. One dramatic example — over 10 million jobs have been recovered since April. By comparison, it took 54 months, from October 2010 to March 2015, for an equivalent number of jobs to be recreated in the aftermath of the Financial Crisis. [data from the US Bureau of Labor Statistics]

We are pleased to present the last stage of our updates and improvements to our monthly newsletter. You will now find a greater emphasis not just on our views of where we just were, but on where we are and where we are headed, with a deeper discussion of the episodic and structural risks we see driving our investment decisions. We also now include a topical discussion of ESG considerations that have emerged as priorities over the period covered by the newsletter.

As always, you will find our newsletters in the Library, available to all.

The US stock market continues to rebound from the pandemic panic-driven lows, with the NASDAQ and S&P 500 continuing to post new all-time highs over the past several weeks. This is prompting investors to question if the current rally can last, or even if it marks the beginning of a new bull market. There are risks that could derail the stock market’s advance ranging from tensions with China, resurging virus hot spots, social upheaval around the country, and the upcoming national elections. The US labor market is also a persistent drag and will not likely have recovered until well into 2021.